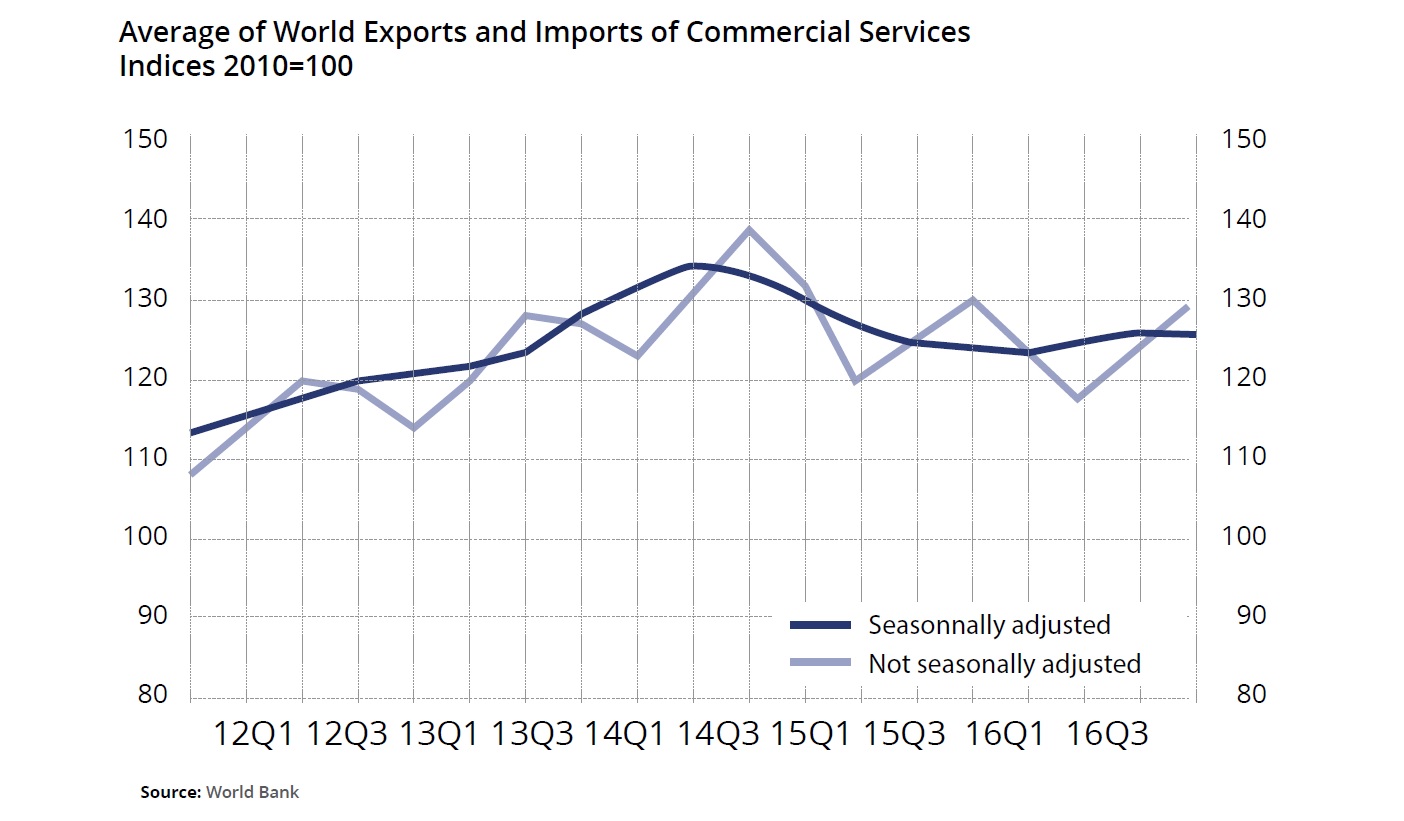

When the IMF published its World Economic Outlook last October, it devoted a lengthy chapter to the slowdown in global trade, a large part of which was attributed to protectionism. The Fund cited data from Global Trade Alert, which detected a ‘steady increase’ in counterproductive trade restraints since 2012, and especially the past three years. Moreover, the year 2015 witnessed the most significant rise in so-called temporary import measures. A seemingly small 2.5% of merchandise goods is affected, but the trend is worrying and the scale of trade barriers has jumped by five-fold since 1990, when globalization was not viewed to be entrenched, or broadly discussed as a phenomenon.

According to the IMF’s calculation, protectionist measures or ‘discriminatory’ actions are worth somewhat more than all other factors in explaining the recent decline in international trade combined. This is ironic, because first, one would more commonly draw a correlation between trade and GDP, and second, the coverage of free trade agreements has been rising rapidly (although such agreements by the number peaked during the 1990s). That is, close to 25% of global flows transpire under free trade accords, compared to 10% some fifteen years ago. Therefore, as trade has become less encumbered in theory, particularly as average import tariffs have declined, it has become more encumbered in practice. Statistical indicators such as sudden product reclassifications, anti-dumping decrees and ‘countervailing duties’ (which have surged, if from a low base) provide a good deal of support for the argument that protectionism is rising, and they are backed up by indirect evidence such as trade lobbyist activity.

If it isn’t surprising that protectionism is on the prowl, you may want to consider some important questions: is this the natural reaction to a slowdown in global growth, meaning that as competition for global supply and demand increases, do countries react by inserting sand in the wheels to ensure their companies are not disadvantaged? Have countries been quietly offsetting the surface level liberalization of trade flows by imposing quiet restraints? Will the situation become worse as economies such as the US and UK become more populist? And, will this lead to the playing field becoming ever more uneven?

Is the Grass Always Greener?

The British government argues that in its post-EU life, it will be free to negotiate trade deals with everyone and everywhere, and that these could be accomplished expeditiously. However, if the world is going to become ever more protectionist, it may find itself shut out from everywhere, because, after all, there is more to trade pacts than simply tariffs, the more complicated discussions being market access and technical standards. If the UK is able to turn its back on free movement from the EU, who is to say that India or Australia, in sensing a labour gap, would not insist that their nationals be able to travel and work more freely in Britain as a quid pro quo in fast tracking an agreement?

Still, there is more than meets the eye when it comes to determining a protectionist intention. For example, what may seem protectionist on paper may be the normal course of events in practice. That is, a large-scale producer in one country may counter an unexpected decline in demand by selling abroad at below its cost of production. The recipient country may in turn impose levies that match the perceived subsidy, and if ineffective, impose non-tariff barriers, which may then be met by further retaliation.

In addition, an unexpected currency devaluation can have unintended medium term consequences in uncertain directions. While resisted at first, policymakers in a country such as Turkey may begin to appreciate the net competitiveness benefits if the pass through to inflation is limited, and subsequently, may steer their currency toward weakness in the future. This would be dissimilar from the ‘beggar thy neighbour’ strategies of the past, because in this instance the initial depreciations were resisted.

With that in mind, few emerging markets have the resources to effectively set the level of their real or nominal exchange rate throughout the business cycle. On the other hand, when foreign producers are priced out of the market after a devaluation, they may have a difficult time recovering their former clients when conditions normalize, either because the domestic producers have used the breathing space to become larger and more of a household name (Ukraine’s poultry producer MHP being one example) or because producers learn to cooperate more effectively with regulators (countries such as Russia often point to ‘phytosanitary’ factors when excluding imports such as Brazilian beef).

Finance ministries also have an incentive to tug in the same direction, because if their agriculture sector faces less competition from abroad, farmers will be more profitable and seek fewer subsidies. Many international trade agreements famously exclude farming and military goods, although according to Global Trade Alert, agriculture is second behind basic metals in being affected by ‘harmful trade measures.’

The Devil’s in the Details

These are complicated issues, admittedly, with no clear-cut guidelines for analysis. If Russia temporarily restricted Brazilian beef imports for particular reasons cited by no other country (while Brazil was negotiating renewed access to the US), its health concerns faded when for geopolitical reasons it no longer found Western European substitutes adequate. If Polish apples similarly fell off the recommended list, Turkish tomatoes (worth an estimated US$250mn per year) soon followed - but for bilateral reasons. Whereas the Russian government signed off on the return of package holidays to Antalya when relations became friendly again, it has been slow to recognize again the quality of Turkish fruits and vegetables.

However, it is not baked in stone that protectionism can move in only one direction, because when economic cycles turn and domestic suppliers cannot fulfil internal demand, governments will face three choices: permit greater access to foreign suppliers on equivalent terms, tolerate inflation unnecessarily that benefits a narrow interest group, or make do with shortages that artificially limit employment and output. The tide often swings back and forth, if over relatively long periods of time, in which public policy favours consumers during one part of the economic cycle and producers another.

Companies and investors react to protectionism and its many forms in different manners. For example, Severstal pre-empted any negative repercussion of souring US-Russian relations when in July 2014 it sold two Midwestern plants while steel prices were relatively high, and it utilized the proceeds to deleverage. By contrast, a complicated corporate- and government-to-government dispute between Algeria and Egypt forced the controlling shareholder of Orascom Telecom to sell his stake to VimpelCom. For some time, this was to the benefit of the holders of equity, but to the detriment of bondholders.

Meanwhile, it is easy for corporates to get caught in the cross-fire. The US Commerce Department and EU Commission more recently concluded that Chinese steel producers were offloading their excess capacity at sub-market prices, but in order to calculate penalties were required to study the entire market. They eventually concluded China was not the only country gaining unfair advantage, and tariffs were eventually imposed on Russian firms as well.

The impact has been relatively muted, though, because the actions applied to narrow sectors such as hot rolled coil and a manufacturer such as NLMK has its own rolling facilities in France and Belgium. The specialized Russian steel producer TMK suffered on the way down, though, because its American division based in Texas was on the receiving end when North America became oversupplied by tubular steel at a time when oil drilling activity was collapsing. Finally, if Norilsk Nickel’s pricing power improved when Indonesia imposed bans on the export of unrefined metals, this fell when the ban was lifted.

More traditional bond financing opportunities have also appeared, as emerging market national champions acquire both to expand footprints and pre-empt possible protectionist actions, whether related to market access or M&A opportunities. ChemChina’s ongoing acquisition of Syngenta and earlier large-scale debt financing is one current example.

From a macro perspective, threats of protectionism can weigh heavily on asset prices; for example, political grandstanding via social media about ‘border taxes’ has caused havoc in the Mexican currency and money markets. The central bank has no exchange rate target, but if currency volatility uproots inflation expectations and negatively affects its credibility, then it must react by raising real interest rates, even if growth prospects are slipping, and even if those border taxes are counter-productive to both countries by definition.

A Trade War Simmering?

A trade war would definitively hurt the struggling state of Michigan, whose number two foreign client is Mexico, to whom it ships nearly as much as the next ten countries combined. In addition, Mexico buys an estimated one million barrels per day of American-produced gasoline. Finally, a Japanese nameplate auto assembled in Tennessee (the Nissan Leaf, for example) with a NAFTA content of 15% and more than 80% Japanese content is viewed to be ‘American,’ but a car completed south of the border and with a far higher US content is viewed to be ‘Mexican.’ The Monterrey-based parts producer Nemak watched its risk premiums rise as investors sell and traders mark down prices just in case, even though an extended and material impact from a trade war on its P&L is more or less tail risk.

Ultimately, the only effective tool for analysing the impact of trade barriers on individual credits is case by case study. Using a common analogy, the implications are more likely to be a drizzle than a thunderstorm, although the decline of the peso to tequila crisis-type undervaluation is becoming the exception that proves the rule.

However, this could be an example of April showers that turn into May flowers, because it is conceivable that through negotiation, the 25-year old NAFTA is modernized in a fashion that benefits all three countries. In addition, Mexico relies on the US for 80% of its exports and the current crisis of confidence shows signs of motivating overdue diversification steps toward other countries and away from a reliance on industries such as autos.